Operation Epic Furry began on February 28, 2026, when the U.S. and Israel launched coordinated airstrikes on Iranian nuclear, military, and leadership targets. In response, Iran closed the Strait of Hormuz on March 2, 2026. This has had a ripple effect throughout numerous industries worldwide, from the energy sector, where 20% of the world's oil and gas supply is suddenly frozen, to healthcare, where patients may have to wait even longer to use an MRI machine.

Overview

The Strait of Hormuz is a 29-mile (54km) wide waterway that separates Iran and the United Arab Emirates (UAE). According to the International Energy Agency (IEA), 20 million barrels passed through the Strait per day in 2025. With this chokepoint cut off from the world, hundreds of millions of barrels of oil have been delayed from reaching their destinations.

- 20% of the world's oil ships through the strait

- 30% of the world's liquid natural gas (LNG) passes through

- 82% of crude oil leaving the Strait is bound for Asian countries

- ~$600bn (£447bn) in energy value passes through each year

The average speed of these transport ships is 10-13 knots (~12–15 mph or 19-24 kmh). That's essentially a person riding their bike from the Strait of Hormuz to their nation's respective ports. Americans need to wait 4-7 weeks for oil tankers to arrive, while the Chinese wait 20-25 days. Therefore, nations closer to the conflict experienced an immediate impact on their oil prices, while those further away, such as North American nations, will experience continued oil shock for 1-2 months after the war ends.

There are limited alternatives to ship oil and natural gas out of the region. There are two major energy pipelines, one in Saudi Arabia that transports gas to the Red Sea, and one in the UAE that sends oil to the other side of the Strait of Hormuz. However, these pipelines move a fraction of oil (7 million barrels per day) compared to oil tankers in the Strait.

The limited movement of oil and reduced oil production have not only raised energy prices but also threatened the affordability of more than 6,000 products produced from oil byproducts.

European Energy, Russia, and Ukraine

For years, Turkey has been quietly executing one of the more sophisticated energy diversification strategies in the world. In the early 2000s, roughly 60% of Turkey's natural gas came from Russia — a dependency that gave Moscow enormous leverage over Ankara's foreign policy. By 2026, Turkey had reduced that share to around 37%, pivoting to Iran, the United States, Azerbaijan, and LNG spot markets. It was a genuine achievement of strategic patience.

The Iran war has now put that achievement at risk — and the reverberations extend well beyond Turkey's borders.

The existing Turkey-Iran natural gas contract expires in July 2026. Under normal circumstances, the two countries would be deep into renegotiation. Instead, Turkey's Energy Minister Alparslan Bayraktar confirmed that no talks have begun. "We haven't started a negotiation during the current circumstances in the region," he told reporters in Antalya.

With the Iran deal in limbo and Iranian energy infrastructure damaged by Israeli strikes, Turkey has been moving to fill the gap. In April, Turkey's state pipeline operator was quietly granted a 10-year license to import liquefied natural gas from Russia — the first time such a long-term license has been extended to Russia in that format, previously reserved only for countries like Algeria and Oman. Turkey already imports Russian gas via the Blue Stream and TurkStream pipelines, which together cover about 35% of its gas supply. Add a long-term Russian LNG arrangement, and Turkey is on a trajectory toward greater energy dependence on Moscow at precisely the moment the West has spent four years trying to pull Europe in the opposite direction.

This matters for the Ukraine war in ways that have gone almost entirely unreported. Russia's economy has been under sustained pressure from Western sanctions since the 2022 invasion. Energy revenues — diminished but not eliminated — remain a critical lifeline. A meaningful increase in gas revenue flowing from Turkey to Moscow is, in practical terms, partial sanctions relief. Turkey has spent the Ukraine war maintaining ties with Russia, refusing sanctions, and positioning itself as a diplomatic intermediary. Turkey is not the only nation extending a lifeline to Russia.

With Iranian and Gulf crude oil suddenly off the table, both China and India have pivoted sharply toward Russian oil to fill the gap. In March 2026, nearly half of India's crude imports came from Russia, roughly double its February share. Chinese crude imports from Russia surged 40% year-on-year in the first quarter. In the first quarter of 2026, 90% of Russia's total crude exports went to China and India.

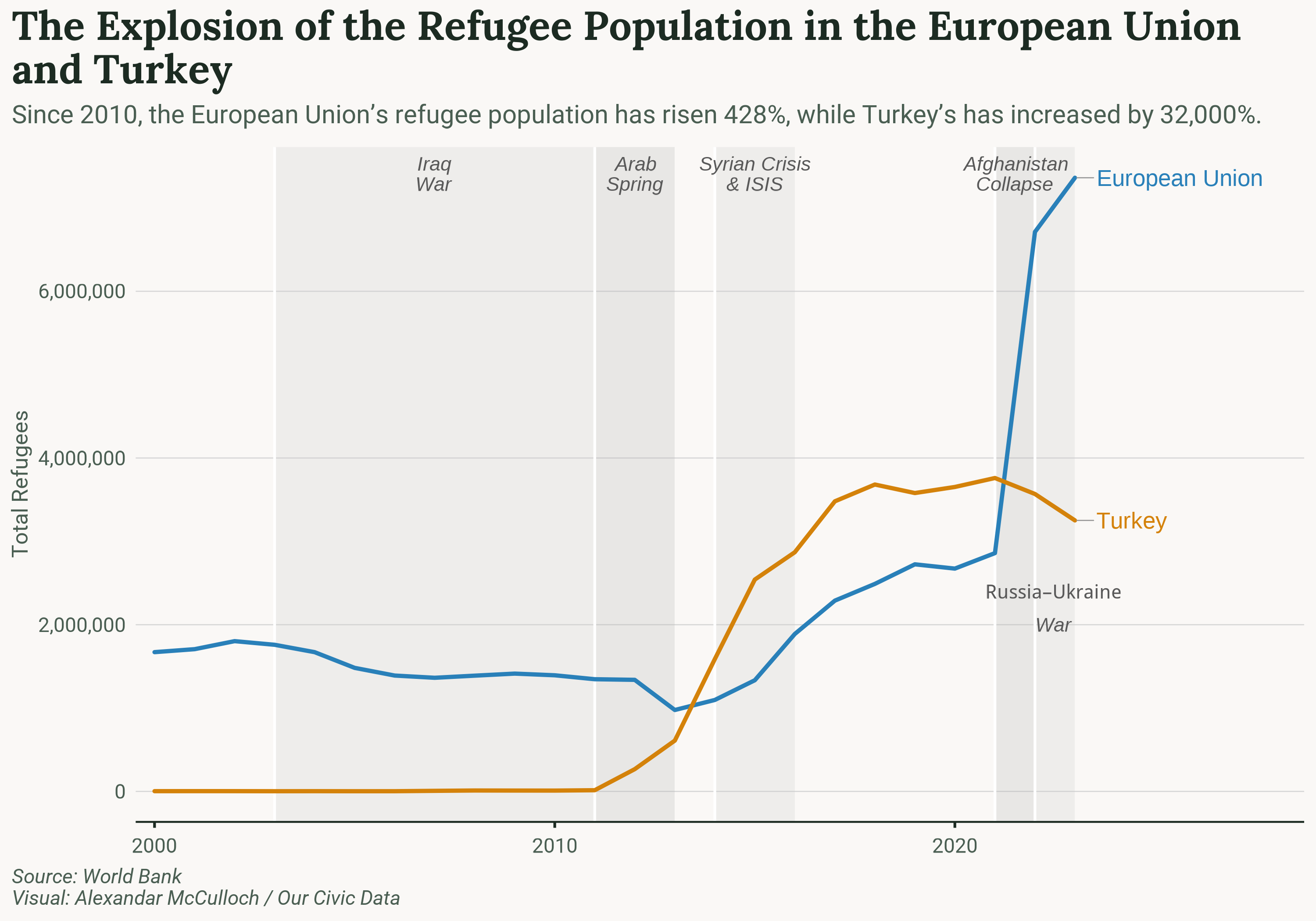

The Refugee Problem

As of April 30, 2026, approximately 3.2 million Iranians have been displaced. In response to the rising number of refugees, neighboring state Turkey has tightened its borders. This is far from the first instance Turkey has had to prepare for a refugee crisis.

Indeed, the 2015 refugee crisis, where 1.3 million refugees poured into Europe, resulted in a landmark agreement between the European Union (EU) and Turkey to limit irregular migrants entering Greece from Turkey (see also EU-Turkey Statement & Action Plan). Turkey accepted the return of the migrants and agreed to take steps to prevent new migratory routes from opening. In return, the EU resettled Syrian refugees from Turkey, reduced visa restrictions for Turkish citizens, and paid 6 billion euros in aid to Turkey for Syrian migrant communities, of which 3 million currently reside in the country.

Turkish officials had expressed concerns over the possibility of a new refugee crisis just days prior to the joint U.S.-Israeli strikes. Officials drafted contingency plans that involve the creation of camps near the border and even entering Iranian territory with the intent to prevent refugee crossings.

There are legitimate political concerns related to the current refugee population. The general sentiment toward Syrians in Turkey has shifted from sympathetic in 2017 to resentful in 2023. The majority of Turks agreed with the statement that Syrians "are victims who escaped persecution/war" (57.8%). By 2023, 50% described them as "people who will cause social and economic problems in our country," with 39% calling them "burdens" (Syrians Barometer 2023, pg. 85). Consequently, President Erdoğan and his AKP party have updated their narratives, from language emphasizing commonalities and brotherhood to advocating for the repatriation of Syrians.

European officials share the same anxieties, with some anticipating a renewed populist backlash, the same backlash that elevated far-right anti-immigrant parties since 2015. The AfD in Germany, for example, is now polling ahead (27% to 24%), with Chancellor Merz's center-right party (CDU). The United Kingdom's center-left Labour party, which achieved a significant victory in 2024, has been polling well below far-right Reform UK since April 2025.

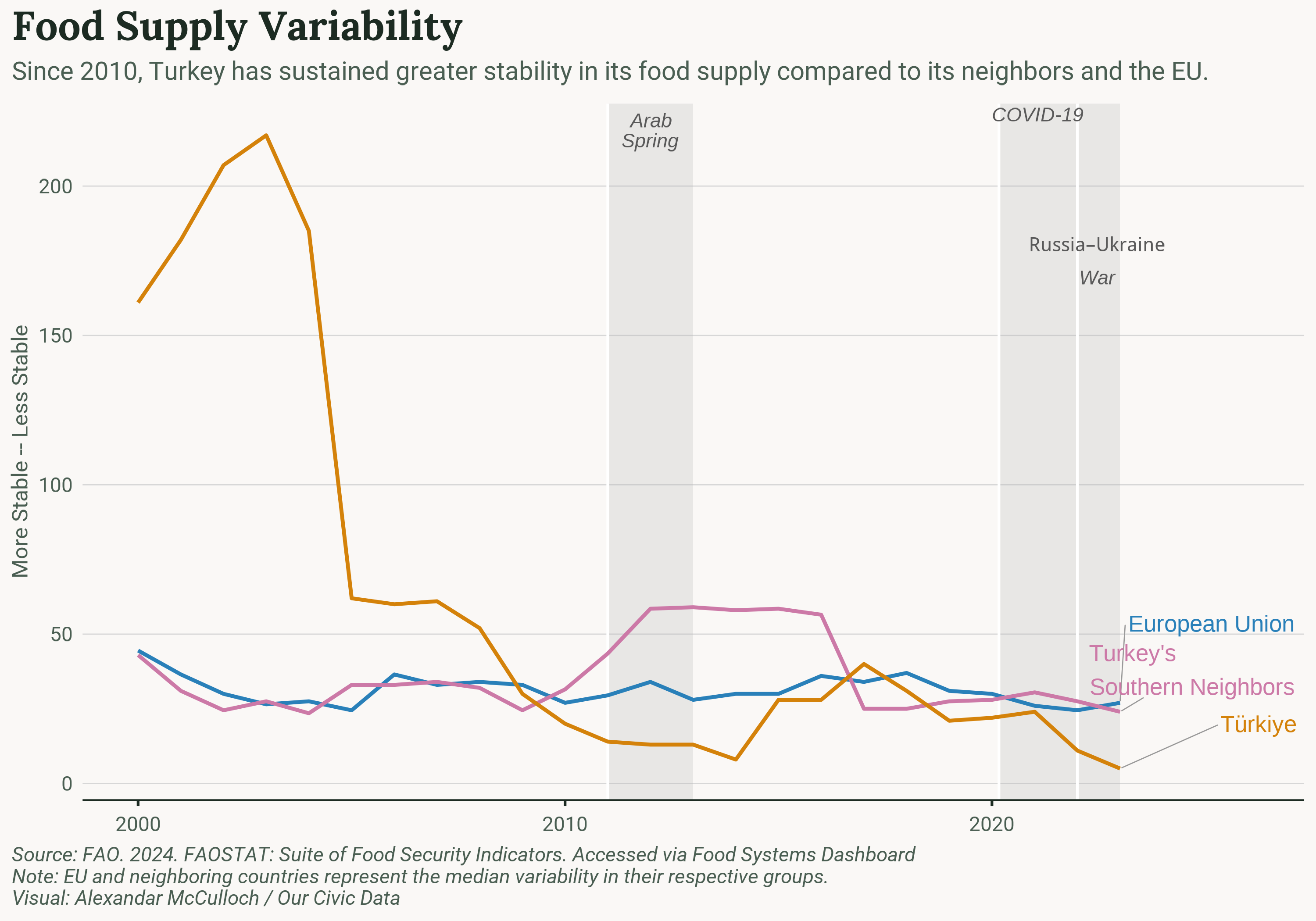

Food Insecurity

War is not a famine. But war can create one indirectly, through disruptions to energy, fertilizer, logistics, and food distribution systems.

Middle Eastern nations have been susceptible to unstable food supply. Since 2016, however, the countries bordering Turkey on its southern borders have sustained little volatility in their food supply, scoring just as well or better than the European Union. This is all based on data from the Food and Agriculture Organization of the United Nations (FAO). Exploration of the data is available on the Food Systems Dashboard, organized by The Global Alliance for Improved Nutrition, Johns Hopkins University, Cornell University’s College of Agriculture and Life Sciences, and The Food and Agriculture Organization of the United Nations.

According to the Food Systems Dashboard, "the ability of the system to maintain a low variability in the supply of food products in the face of shocks is a direct way to assess the system long-term resilience. A resilient food system would be able to keep the variability of food supply low despite being hit by shocks. Therefore, the lower the food supply variability, the better."

Nations with the most volatility are most susceptible to the shock of the Iran war, since the war will disrupt five core components that drive food costs: crop yields, processing and packaging, supply chains, labor costs, and retail markups. The Iran war has its heaviest hand on the first three, and it is pressing on all of them simultaneously.

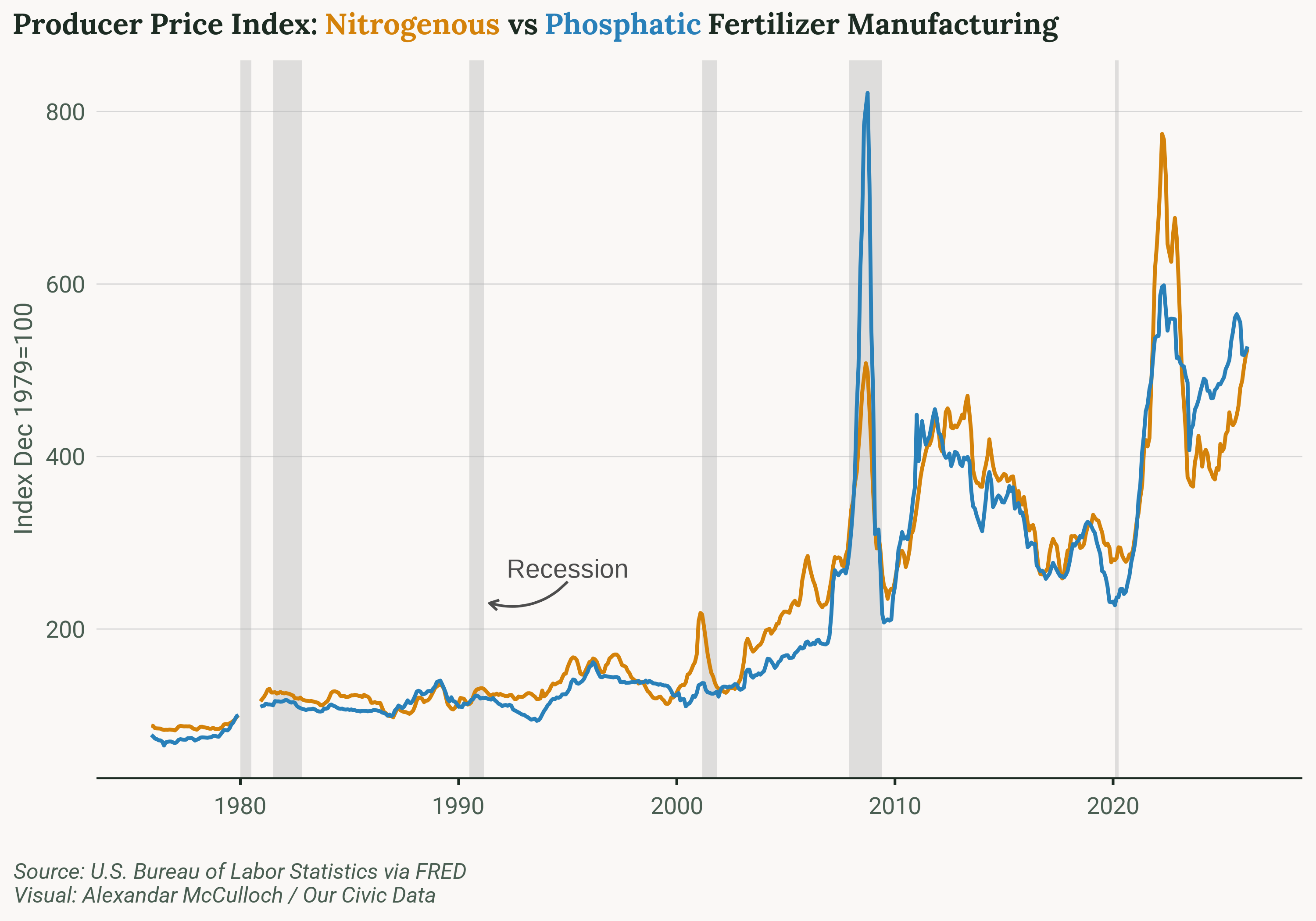

Crop Yields: The Fertilizer Problem

Natural gas is not just a fuel. It is the primary feedstock for nitrogen-based fertilizers — the compounds that allow modern agriculture to produce the crop yields the world now depends on. The Strait of Hormuz closure disrupted both the natural gas supply itself and the export routes for urea and sulfur, the Gulf's two dominant fertilizer components. Gulf countries supply 45% of globally traded sulfur and nearly half of seaborne urea.

Fertilizer prices spiked 49–50% for urea and ammonia just as the Northern Hemisphere spring planting season began. About 80% of American farmers had locked in their fertilizer prices the previous fall; the 20% who hadn't faced a stark choice between absorbing crushing new costs or planting less. The USDA estimates corn and wheat acreage will each fall roughly 3% in 2026. When farmers plant less, they harvest less. When they harvest less in the fall of 2026, global grain stocks tighten heading into 2027.

The regions already most exposed are not the United States or Europe. The FAO has identified India, Bangladesh, Sri Lanka, Egypt, Sudan, and sub-Saharan Africa as the hardest hit by fertilizer shortages. East African nations, entering their planting season as the crisis deepened, found themselves unable to source the inputs they needed at prices their farmers could afford. In Somalia, some essential commodity prices had already risen at least 20% since the war began. Sudan — where 80% of wheat is imported — faces a direct and immediate impact on the staple that feeds its population.

Packaging and Processing: The Plastic Problem

The connection between oil and a box of cereal is not obvious, but it is direct. Plastics are made from naphtha, a crude oil derivative. Naphtha prices in Asia have surged from roughly $108 per ton to more than $400 per ton since the war began. Polyethylene — the plastic in the packaging around almost every product in your grocery store — is up 40–50%. Those costs have not yet fully reached retail shelves. Price changes move through the manufacturing and distribution chain with a lag of four to eight weeks. The grocery price increases most consumers will see in May and June 2026 reflect input costs locked in during March and April.

Food packaging is not incidental to food security. Without packaging, perishables cannot travel from farm to processor to retailer. When packaging costs surge, the cost of every food product that requires it surges too, compounding the upstream fertilizer shock with a downstream distribution shock.

Supply Chain: The Distance Problem

The Strait's closure does not just cut supply; it reroutes existing supply along dramatically longer paths. Under normal circumstances, the World Food Programme procures food in India, ships it to Salalah in Oman, then to Jeddah in Saudi Arabia, and finally to Port Sudan. With the strait closed, that same cargo now travels an additional 9,000 kilometers; the equivalent of a coast-to-coast trip across the United States and back, adding roughly 25 days to shipping times and proportional increases in fuel costs.

Healthcare Technology

Helium is the second most abundant element in the universe. On Earth, it is vanishingly rare — found only in trace quantities within certain natural gas deposits, impossible to synthesize, and notoriously difficult to contain. It leaks through almost any seal at a rate of 0.1 to 1 percent per month. It cannot be manufactured. And it is the only substance cold enough to keep the superconducting magnets inside an MRI machine operating.

The Iran war has disrupted roughly one-third of global helium supplies — primarily because of what happened at Ras Laffan Industrial City in Qatar on February 28. Iranian missile strikes on the facility caused three fires and destroyed approximately 17% of Qatar's LNG export capacity. Helium is extracted as a byproduct of LNG processing. You cannot produce one without the other. When the LNG plant stops, the helium stops with it.

The supply chain is long and slow. Suppliers pump most of the world's helium into 11,000-gallon cryogenic containers that are loaded onto trucks and craned onto cargo ships. Helium that shipped out of Qatar right before the war started may still be on its journey. The helium shortage is, right now, a tsunami visible on the horizon rather than one already at shore. But it is coming. "There's no physical shortage right now at the end-user level," as one helium consultant put it. "It's kind of like a nice sunny day on the beach, but you heard there's a tsunami out there. You've got to get out of the way."

Some hospitals already haven't. Saskatchewan's provincial health authority has been warned by its supplier that its helium allocations "will be reduced temporarily by 50 percent." Air Liquide, Canada's largest liquid helium distributor, has declared force majeure and sent notices to some of its customers, warning that their supply is being cut by 50 percent, with prices hiked. The hospitals receiving those notices are not panicking yet — most have several months of inventory — but they are doing quiet triage: assessing which MRI machines are oldest and consume the most helium, and prioritizing refills accordingly.

For radiology departments already managing waiting lists and diagnostic backlogs, reduced MRI availability could mean delayed cancer diagnoses, postponed surgical planning, and longer patient pathways through secondary care. To make matters worse, hospitals are competing for a shrinking supply.

Helium is essential for the chip industry, which, propelled by the AI boom, is one of the most powerful forces in the global economy, underpinning companies from Nvidia to Google to Meta and buoying over a third of U.S. GDP. The semiconductor industry has recently overtaken MRI scanners as the world's largest helium consumer. When supply tightens, hospitals and chip manufacturers bid against each other on the open market. Bidding wars have more than doubled helium prices on the open market.

One encouraging note is that suppliers prioritize critical applications during shortages. Medical MRI machines will get special priority over other industries. However, the long-term picture is less optimistic. Energy analysts estimate it could take up to five years to restore full production capacity at Ras Laffan. The regions that will feel the shortage first and most acutely are Japan, Singapore, South Korea, and Taiwan — home to the world's most advanced chip fabrication facilities and heavily dependent on Qatari helium. Their MRI machines and their chip fabs are competing for the same gas, from the same compromised source, with no quick fix in sight.

The broader consequence of the Iran war is not confined to the battlefield or even to energy markets. It is the emergence of interconnected shortages — fuel, fertilizer, shipping capacity, helium, medical access — whose effects compound across borders and industries long after the fighting itself subsides.

One strait. Six thousand products.

The unexpected costs of war.

The Strait of Hormuz is 21 miles wide. Through it flows 20% of the world’s oil — but also the feedstocks for plastics, fertilizer, helium, and EV batteries. Click any node or tab to trace how a missile strike on a Qatari gas plant ends up delaying your MRI scan.

The Hormuz Domino Effect

The Strait of Hormuz is 21 miles wide. Through it flows 20% of the world’s oil — but also the feedstocks for plastics, fertilizer, helium, and EV batteries. Every node above is connected. Select one to trace its chain.

20% of oil supply 1/3 of fertilizer trade 1/3 of helium supply 30% of methanol trade

Subscribers can submit a topic suggestion below. Sign up to suggest what I should cover next!